I write a lot about relationships. Relationships are important. Unless your parents had a great relationship and they educated you on this topic, you probably weren’t well-equipped for healthy relationships. It’s not a topic that usually gets covered well at school or church.

When people aren’t educated about relationships, they form bad habits, they get hurt, and maybe even damage their futures.

But if there’s one topic that gets addressed even more poorly than relationships, it’s money.

If your parents don’t teach you good money habits, you probably won’t learn them anywhere else. In most countries, it’s not part of the school curriculum and it definitely doesn’t get spoken about at church (beyond an encouragement to put some money in the collection plate each week).

Like relationships, if people aren’t educated about money they make mistakes, they hurt themselves financially, and even damage their futures.

I’m by no means an expert when it comes to money management, but I have done what I think every young adult should do, which is set aside some time to educate myself about money. Here are five money habits every Christian young adult should have:

1. BE INTENTIONAL ABOUT YOUR SPENDING

When it comes to spending, a lot people can feel like they’ve only got two options. Option 1 (the thing they are supposed to be doing), is meticulously adhering to a detailed budget in every aspect of their life, recording every purchase, and reviewing their spreadsheets regularly to ensure they’re not going over their estimated monthly spend for dental floss.

Option 2 (the thing they’re actually doing) is the “ignorance is bliss” approach. Money goes into an account, it comes out of that account for rent, food, etc. and if there’s anything left over, it gets spent on whatever is at the top of your wish list.

For several years, I made the mistake of oscillating between the two. I would try Option 1, only to lose motivation within a month and default to Option 2, only to get frustrated by my total lack of financial progress and return to Option 1, and so on.

The solution, I’ve found, is somewhere in between – coming up with a budget that allocates different portions of your income to different places, but then spending it without much further thought. No spreadsheets, no zealously recording every purchase, no monthly dental floss budget.

Scott Pape, one of my favourite authors on this subject, recommends that if you’re on a full-time income, no more than 60% of that income should go to weekly expenses, around 30% should go savings, and 10% you should spend on whatever you want.

If you’re a student, it might be that 80% of your weekly student allowance/loan goes to weekly expenses, you save 10% and spend 10% on whatever you want.

A lot of these finance authors don’t recognise the importance that Christian’s place on giving to church and charity, so to incorporate this, a possible breakdown could be 60% of your income on weekly expenses, 15% to savings, 10% to giving, 5% to investment, and 10% on whatever you want.

The point is having a strategy that allows you to make progress financially, but without it consuming your life.

With this in mind, it’s important to automate how your money is allocated to these different places. To do this, I set up a couple of everyday accounts with my bank for “weekly expenses” and “whatever I want,” and three savings accounts for “saving,” “giving” and “investing.” Every week when I get paid, the money goes into my weekly expenses account, and then the allocated proportions are automatically transferred out to the other 4 accounts.

After that, I don’t have to think about it. Food and rent get paid for by everyday expenses, I can spend every dollar in my “whatever I want” account, and I don’t have to feel guilty about every purchase, because I know that I’m saving, giving and investing in the background.

2. LIVE WITHIN YOUR MEANS

We live in a culture of buy now, pay later. More than 50% of millennials now report using payment options like Afterpay, which allows you buy something, and then pay for it later in four fortnightly interest-free payments.

The actual terms of these Buy Now Pay Later (BNPL) arrangements aren’t so bad – they beat paying 20% interest on a credit card. But the habit they reinforce is problematic: if you can’t afford it now, no stress, rely on credit and pay it back later.

The results of this bad habit were clearly seen in a review conducted here in Australia, where I live, which found that one in six millennials using Afterpay (or it’s equivalents) was in financial strife: getting overdrawn, delaying bills, or borrowing more.

Everyone knows that if you want to lose weight, there are two simple steps: eat healthy and exercise. We can complicate the process with fad diets, workout routines and superfoods we want, but the simple, hard, effective thing to do is eat healthy and exercise.

Living within your means is the “eat healthy and exercise” of the personal finance world. Virtually every money management book boils down to this principle: if you don’t have the money for it in your bank account, you can’t afford it.

If you can’t afford it, you’ve got three options (1) save for it, (2) buy a cheaper version, or (3) don’t buy it. But don’t (1) get a loan for it (with the exception of a mortgage or a student loan), (2) put it on a credit card, or (3) buy it with Afterpay.

Seriously, it’s tempting to complicate this – “but I can afford the repayments”, “but 2% interest on that car loan is virtually nothing”, etc. etc. But if you want to avoid financial strife, the simplest way is to live within your means.

WANT RELATIONSHIP

GAME CHANGERS?

Subscribe to the newsletter for weekly relationship advice,

date ideas and the latest blog posts.

3. START INVESTING

If you’ve never learnt much about investing, you might think that the stock market is something reserved for people with degrees in finance or economics, who read the Wall Street Journal every morning.

However, with zero business knowledge and as little as a few hundred dollars, you can start investing. The way most people do this is through Exchange Traded Funds (ETFs) or Index Funds.

In simple terms, ETFs and Index Funds typically track the performance of an index of the largest publicly traded companies on the stock market. For example, the S&P 500 Index tracks the performance of the 500 largest U.S. publicly traded companies.

At this point, you might be thinking “too much jargon for me,” but stick with me. If you’re in your twenties, this is a way that you can make tens or even hundreds of thousands of dollars for very little work. That sounds like a scammy pop-up you’d get while trying to illegally stream your favourite TV series, but it isn’t. It comes down to one thing: compound interest.

Starting to invest now, even just a small amount every month, is the simplest and most sure-fire to be in a great financial position later in life. The amount you invest will earn interest, which can then be automatically reinvested, meaning that you’ll earn more interest, which can then be automatically reinvested to earn MORE interest.

I’m not one for including graphs in my blog posts but driving this point home calls for a few graphs.

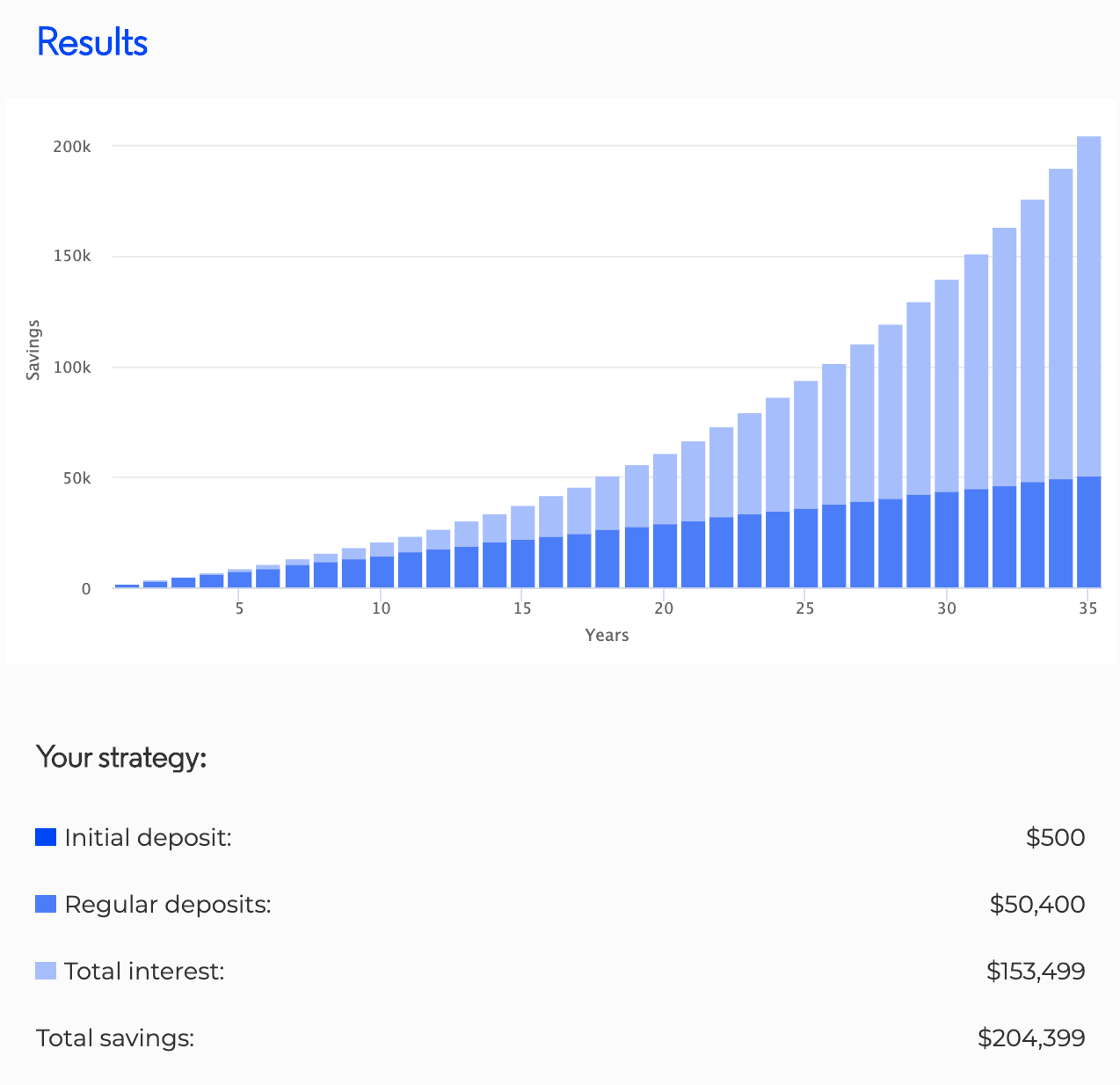

Let’s say you’re 25 years old, you deposit $500 initially into an ETF, and you top that up with $30 per week. We’ll assume you’re earning 7% interest per year (adjusted for inflation, the historical average return for the S&P 500 has been around 7%). You don’t touch it until your 60th birthday, which is 35 years.

Taken from: https://moneysmart.gov.au/budgeting/compound-interest-calculator

By the time you’re 60, that amount will be $204,399, and a whopping $153,499 will be interest (money you haven’t put in yourself).

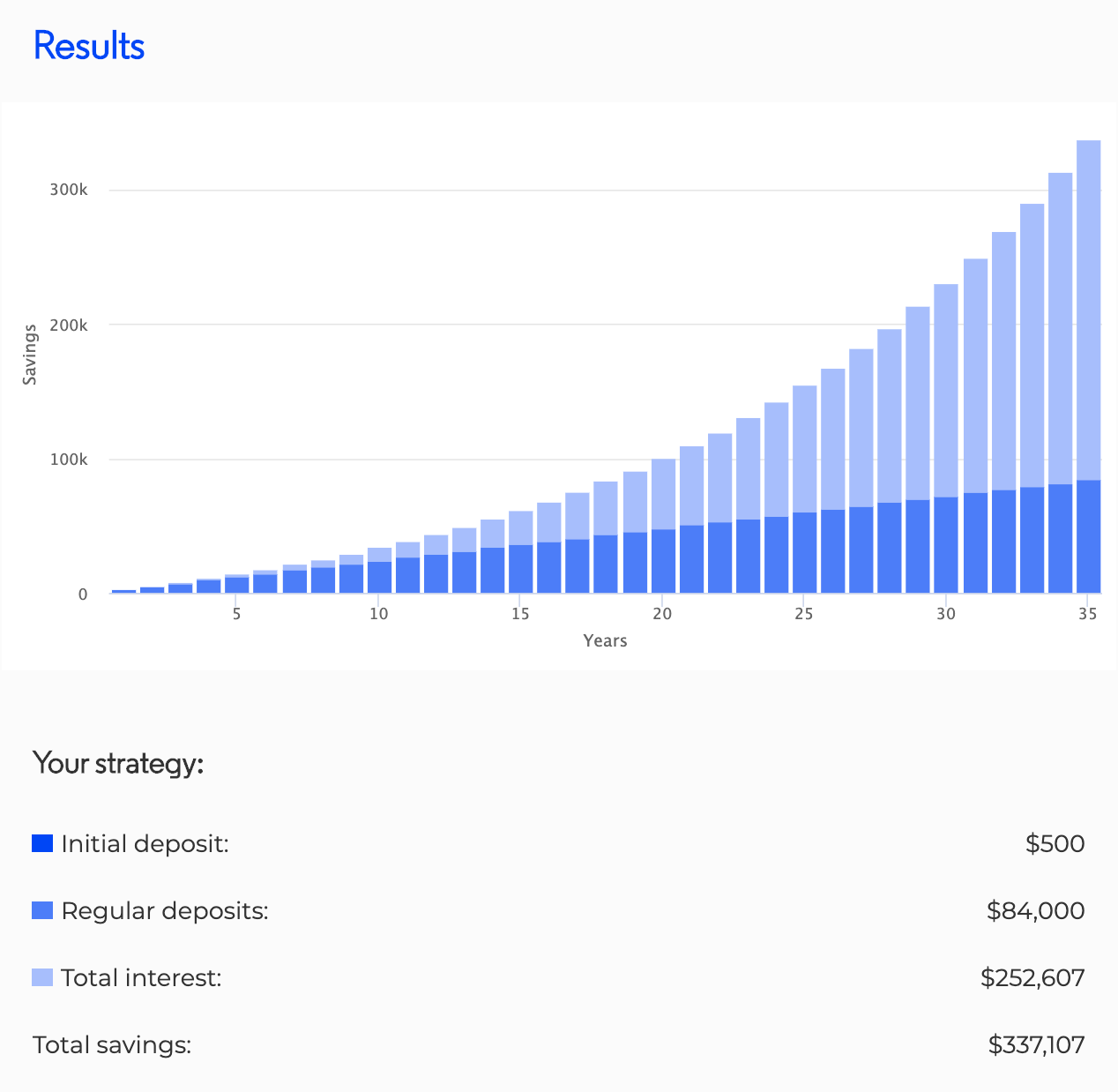

Let’s say you can afford a bit more, and you put aside $50 per week for investment:

That’s $337,107 by the time you’re 60, and $252,607 of that is interest.

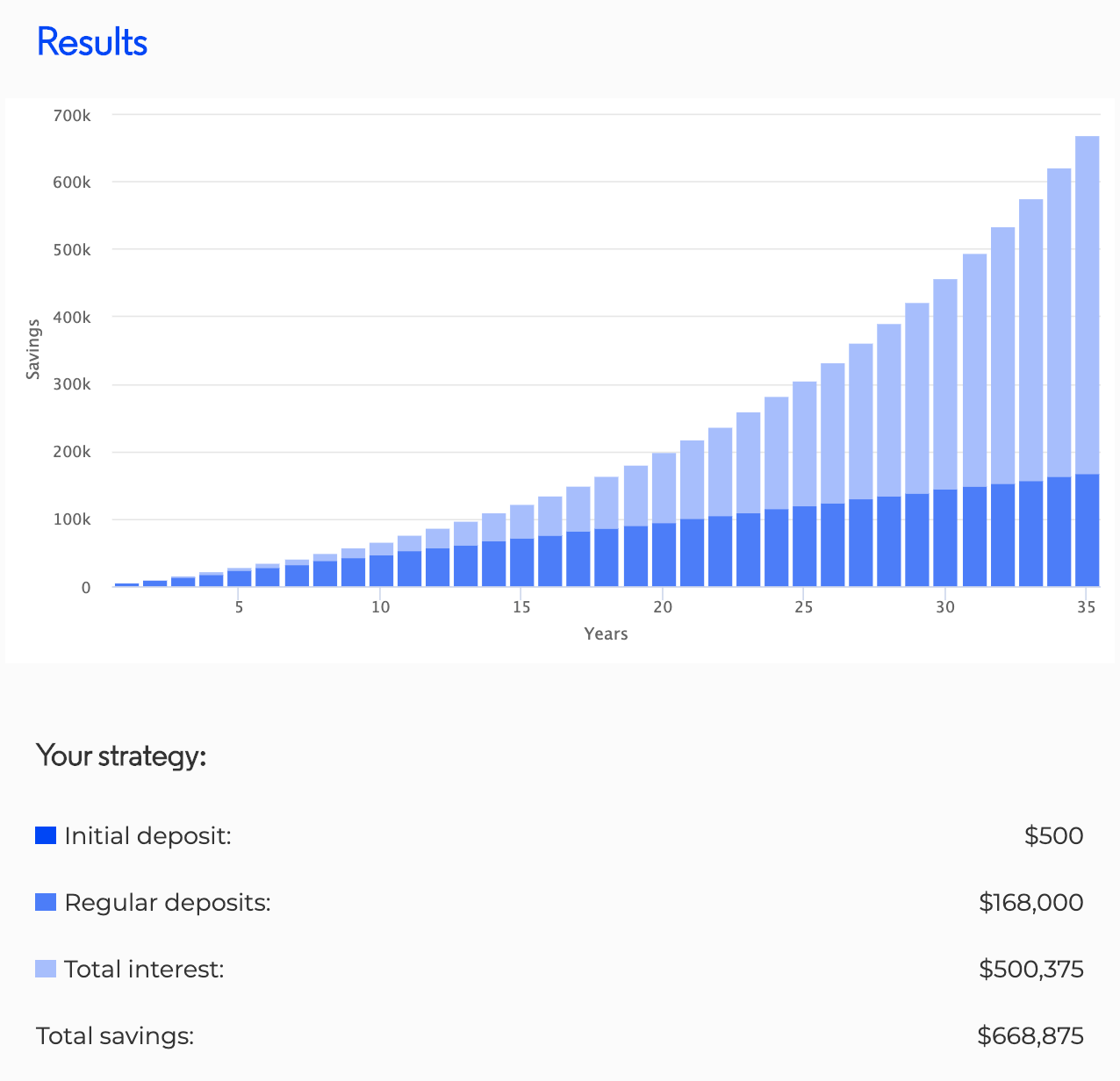

Want to get more serious? Let’s bring it up to $100 per week:

In 35 years, you’ve got $668,875, with a whopping $500,375 of that being earned from interest.

If you’re living in a country like Australia or New Zealand, where money is automatically deducted from your salary into a superannuation fund, the good news is that you’ve already got a fund compounding away for you. But consider having self-managed investments on top of this. I invest another 5% of my income into ETFs.

If you live in a country that doesn’t have these kinds of mandated retirement funds, it’s all the more important that you take long-term investing seriously.

I’m just scratching the surface here. I’d encourage you to take a few evenings to research ETFs and get the best recommendations for your personal situation and the country you live in. This is too valuable a habit not to educate yourself about.

WANT RELATIONSHIP

GAME CHANGERS?

Subscribe to the newsletter for weekly relationship advice,

date ideas and the latest blog posts.

4. GIVE TO CHURCH AND CHARITY

Contrary to what the Boomer on your church finance committee might tell you, Millennials aren’t all self-obsessed spenders.

One survey by the Evangelical Council for Financial Accountability (which absolutely sounds like an organisation from a Dystopian Evangelical future) surveyed more than 16,500 people and found that almost all of the millennials surveyed (92%) had given to their church in the past few years.

Another study found that 60% of millennials donate an average of $481 to non-profits every year. Given that, on average we have more debt and less income than any other generation before us, that’s not half-bad.

However, my concern is that generally speaking, we as millennials don’t have a habit of giving. We give to the occasional crowdfunding campaign and worthy cause, but most of us don’t give monthly to church and/or charity.

Why should we? Well, let me start by contradicting the mega-church pastor in your local area and say that strong arguments can be made that Christians today aren’t required to adopt the Israelite practice of tithing (giving 10% of one’s income to the church).

However, the Bible is abundantly clear that we should support those you preach the gospel (Matt. 10:10; Luke 10:7; 1 Cor. 9:6–14; 1 Tim. 5:17–1) and be generous to those in need (Matt 25:34-40; 1 Tim 6:17-19; and especially 2 Cor 8-9).

For me, it comes down to this – Jesus said, “for where your treasure is, there your heart will be also” (Matt 6:21). I want my heart to be focused on (1) doing God’s will and (2) helping people, especially those less fortunate than I am.

At my funeral, all I want people to say is “Sam lived his life for God and for others.” That’s it. So, in the past few months, I’ve made it a priority to give a portion of my income to the church that I’m a part of, and another portion to charity.

If the thought going through your mind right now is “I just can’t afford to,” I want to challenge that aggressively. Because I get it. A year ago, that was my excuse. I was on a ministry wage substantially lower than the average wage here in Australia, I was paying off debt, and also saving for a wedding. And to say that I couldn’t afford to give was a bare-faced lie.

Sure, I couldn’t afford to give much, but if I had been willing to make it a priority and cut costs in a couple of places, I could afford to give something.

Shortly after Renée and I got married, we decided to make this a priority in our lives, and it has been a game-changer. Not because “blessings are raining down on us” like that mega church pastor will tell you they will. But because in this small way, we recognise God’s sovereignty over our lives, we actively build up the church that we are a part of, and we know that we’re doing something to help people.

We’ve only been doing this for a few months, and I can tell you, I don’t ever want to stop. I want to do everything I can to give more. Start small if you have to – start as small as $10 per month. But know that this habit has the power to dramatically change your life, while positively changing so many other lives as well.

5. EDUCATE YOURSELF

As you’ve hopefully noticed by now, all of the habits in the blog post are about long-term investments (both literally and metaphorically).

Being intentional about your spending is about automating positive financial habits and setting you up to navigate the increased expenses and (hopefully) increased income of later adult life. Living within your means is about protecting you from debt that could cripple you financially. The benefits of investing should be self-explanatory, while regular giving is a habit that can allow you to do an incredible amount of good over your lifetime.

Underlying all of these habits is the need to educate yourself about personal finance, and it is a need for our generation. One study found that only 24% of millennials are demonstrate basic financial literary.

Educating yourself is probably the best long-term investment there is. If you learn a few important money management principles in your twenties and build the right habits, then over the next 40+ years, it’s going to enormously beneficial for your life.

You don’t need to read a new personal finance book every month, but you should make it your goal to read a couple.

After reading just two solid personal finance books, I’d conservatively estimate that the knowledge I gained from them saves me around $50 per month. I’m 26 years old. That’s $20,400 by the time I’m 60. If I invest that $50 saved (which is exactly what I’m doing) it’s $76,955 by the time I’m 60. For reading a couple of books! Imagine if your high-school book report had that kind of cost:benefit ratio.

This doesn’t even factor in all the extra money I’ll be able to make, through investing and career strategy, which I didn’t know the first things about prior to reading these books. If you’re looking to get started, these are the three I’d personally recommend:

The Barefoot Investor by Scott Pape (written in an Australian financial context).

I Will Teach You To Be Rich by Ramit Sethi (two versions, one written in a US financial context, the other in a UK context. Yes, I know the title sounds scammy but trust me, it’s a great book).

The Total Money Makeover by Dave Ramsey (written in a US financial context).

Building good habits around money isn’t easy. It demands time, energy, and even a certain degree of sacrifice. In the process, you’ll probably also have a few uncomfortable moments of confronting past money mistakes. But if you’re willing to start today, these habits have the potential to be incredibly beneficial over the course of your lifetime.

For most of us, this Chinese proverb sums it up well “The best time to plant a tree was 20 years ago. The second-best time is now.”

–

Disclaimer: This information is general in nature and does not take into account your personal financial situation. It is for educational purposes only, and does not constitute formal financial advice. You should always seek personal financial advice that is tailored to your specific needs.